U.S. vs. China AI Race: The Battle for Global Technology Supremacy

The intensifying competition between the United States and China over artificial intelligence (AI) is not merely an extension of their long-standing trade disputes; it is a critical battle that could reshape global power dynamics. It is the space race of the 21st century: A competition between the United States and China to develop the most powerful artificial intelligence tools is at a critical point.

As AI becomes the defining technology of our era, the race between these two superpowers has evolved from economic competition into a matter of national security, technological sovereignty, and global influence. The stakes couldn’t be higher, the winner of this AI race will likely dominate the global economy for decades to come.

But who’s actually winning? The answer is more complex than headline grabbing statistics might suggest. The United States maintains an edge in foundational technology and research, while China excels in implementation and scaling. This dynamic creates a complex competitive landscape where success in one area does not necessarily translate to dominance in the broader AI domain.

Current State of the AI Race: Key Metrics

Investment and Funding Comparison

The financial commitment to AI development tells a compelling story about each country’s strategic priorities and capabilities.

| Investment Category | United States | China | Analysis |

|---|---|---|---|

| Total VC Funding (2025) | $178 billion (57% global) | ~$45 billion | US leads by 4:1 margin |

| AI-Specific VC Funding | 42% of US VC goes to AI companies | $120 billion cumulative in AI ecosystem | US higher annual flow, China higher cumulative |

| Government Investment | Federal: ~$25 billion annually | Government-led investment likely exceeds US federal and state investment | China leads in state funding |

| AI Companies Funded (2025) | 1,073 AI companies funded | ~400 estimated | US leads 2.5:1 in new startups |

Research and Development Leadership

An EU report found that 73% of large language models are developed in the US and another 15% in China, highlighting America’s current dominance in foundational AI research.

Research Output Comparison:

- AI Research Papers: China publishes more papers (volume), US produces higher-impact research (citations)

- AI Patents: China leads in patent filings, US leads in patent quality and implementation

- University AI Programs: US universities dominate global AI rankings

- Corporate R&D: US tech giants outspend Chinese counterparts on pure research

Talent and Human Capital

| Talent Metric | United States | China | Key Insight |

|---|---|---|---|

| AI Researchers | ~50,000 active | ~40,000 active | Close competition |

| Top AI Talent | 60% of world’s top AI researchers | 20% of world’s top AI researchers | US significant lead |

| International Talent | Attracts global AI talent | Primarily domestic development | US advantage in brain drain |

| AI Education | 400+ universities with AI programs | 300+ universities with AI programs | US leads in quality |

Strategic Advantages: Where Each Country Excels

1. United States: Innovation and Ecosystem Leadership

Foundational Technology Dominance: The US maintains clear advantages in the fundamental technologies that power AI advancement:

- Semiconductor Design: Companies like NVIDIA, AMD, and Intel dominate AI chip architecture

- Cloud Infrastructure: AWS, Microsoft Azure, Google Cloud provide global AI compute platforms

- Software Frameworks: TensorFlow, PyTorch, and other key AI development tools are US-originated

- Large Language Models: GPT series, Claude, Gemini, and other leading models are US-developed

Innovation Ecosystem: The Silicon Valley model of innovation creates systematic advantages:

- Risk Capital Availability: Mature venture capital ecosystem with AI expertise

- Talent Mobility: Engineers and researchers move freely between companies and universities

- Entrepreneurial Culture: Strong support for AI startups and rapid scaling

- Academic-Industry Collaboration: Seamless partnerships between universities and tech companies

Market Access and Scale:

- Global Market Reach: US AI companies serve worldwide markets from inception

- Enterprise Adoption: American businesses lead in AI implementation and spending

- Regulatory Environment: Generally supportive of AI innovation with measured oversight

2. China: Implementation and Scale Advantages

Manufacturing and Implementation Excellence: China leads the world in industrial robot installations: Chinese manufacturers purchased half the global market share in 2025, and the country’s robots per employee significantly exceeded the global average.

State-Directed Investment:

- Long-term Planning: 5-year and 10-year AI development plans with massive resource allocation

- Infrastructure Development: National AI computing centers and data networks

- Policy Coordination: Unified government approach to AI development and deployment

Data Advantages:

- Population Scale: 1.4 billion people generate massive datasets for AI training

- Data Collection: Fewer privacy restrictions enable comprehensive data gathering

- Government Data: Access to extensive government datasets for AI training

Application-Focused Approach:

- Smart Cities: Leading implementation of AI in urban planning and governance

- Surveillance Systems: Advanced facial recognition and monitoring technologies

- Mobile Payments: AI-powered financial services with massive user bases

- Manufacturing AI: Industrial automation and smart factory implementations

Investment Trends and Strategic Priorities

U.S. Investment Patterns

Private Sector Leadership: The venture capital funding in generative AI startups witnessed an unprecedented surge in the first half of 2025, reaching $15.7 billion. This represents a 2,100% increase compared to the total investment of $581 million in generative AI startups in the full year 2019.

Key Investment Areas:

- Foundation Models: Large language models and multimodal AI systems

- AI Infrastructure: Computing platforms, chips, and development tools

- Enterprise AI: Business applications and productivity tools

- AI Safety and Alignment: Research into controllable and beneficial AI

- Defense AI: Military and national security applications

Corporate Investment Leaders:

- Microsoft: $13+ billion in OpenAI, Azure AI services

- Google/Alphabet: DeepMind, Bard, AI research divisions

- Meta: Reality Labs, LLaMA models, AI infrastructure

- Amazon: AWS AI services, Alexa, robotics

- Tesla: Autonomous driving, robotics, manufacturing AI

China’s Investment Strategy

Government-Led Coordination: Government VC funds often invest in AI firms with weaker initial software production than firms receiving private VC funding, but provide strategic coordination and long-term support.

Priority Investment Sectors:

- Autonomous Vehicles: Leading global investment in self-driving technology

- Smart Manufacturing: Industry 4.0 and automated production systems

- AI Chips: Domestic semiconductor development to reduce US dependence

- Facial Recognition: Security and surveillance applications

- Smart Cities: Urban AI infrastructure and governance systems

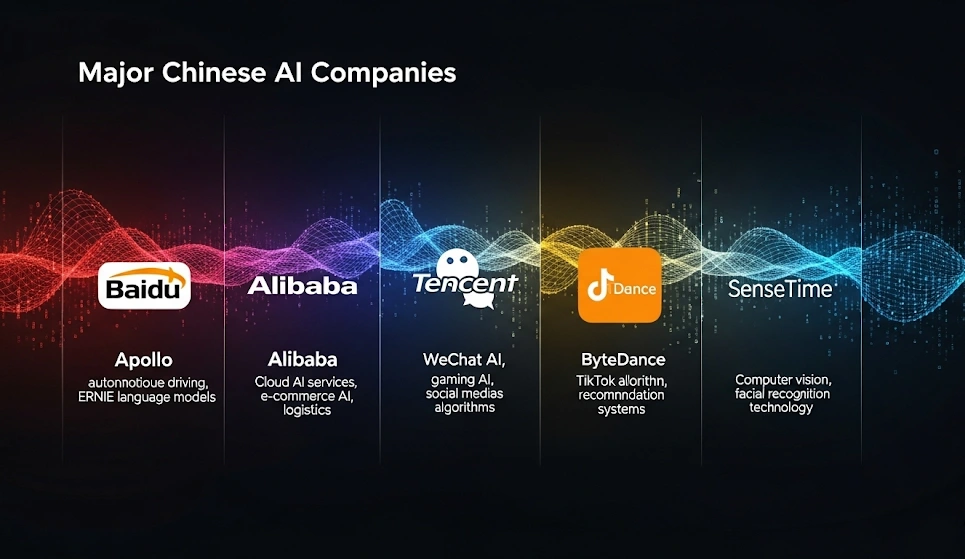

Major Chinese AI Companies:

- Baidu: Apollo autonomous driving, ERNIE language models

- Alibaba: Cloud AI services, e-commerce AI, logistics

- Tencent: WeChat AI, gaming AI, social media algorithms

- ByteDance: TikTok algorithm, content recommendation systems

- SenseTime: Computer vision, facial recognition technology

Competitive Dynamics: Current Battlefield Areas

Semiconductor and Hardware Competition

Current Situation: The US maintains dominance in AI chip design, while China focuses on domestic manufacturing capabilities to reduce dependence on American technology.

Key Developments:

- US Export Controls: Restrictions on advanced semiconductor exports to China

- China’s Response: Massive investment in domestic chip manufacturing

- TSMC Factor: Taiwan’s role as critical semiconductor manufacturer for both countries

- Alternative Architectures: Exploration of quantum computing and neuromorphic chips

Large Language Models and AI Capabilities

Performance Comparison: While US models like GPT-4, Claude, and Gemini lead in general capabilities, Chinese models are rapidly closing the gap in specific applications.

Chinese Model Progress:

- Baidu’s ERNIE: Competitive performance in Chinese language tasks

- Alibaba’s Qwen: Strong multimodal capabilities and reasoning

- ByteDance’s AI: Advanced recommendation and content generation systems

- Deepseak AI: A pioneering AI research company dedicated to delivering high-performance, cost-efficient language models.

Data and Privacy Considerations

Competing Approaches:

- US Model: Privacy-conscious development with opt-in data collection

- Chinese Model: Comprehensive data collection for AI training and applications

- Regulatory Impact: GDPR, AI Act, and other regulations affect development strategies

Geopolitical Implications and Global Impact

Alliance Building and International Influence

China’s plan focuses on leading global AI governance, while the US takes a competitive approach with the goal of market dominance. Global Majority countries could view the US approach as confrontational and may hesitate to increase their technological dependence.

U.S. Strategy:

- Allied Cooperation: Partnership with EU, Japan, South Korea, Australia on AI development

- Export Controls: Technology restrictions to maintain competitive advantages

- Standard Setting: Leadership in international AI safety and ethics standards

Chinese Strategy:

- Belt and Road AI: AI technology exports to developing countries

- South-South Cooperation: Alternative to Western AI frameworks

- Global Governance: Influence in international AI policy discussions

Military and National Security Applications

Defense AI Competition: Both countries recognize AI’s critical importance for future military capabilities:

U.S. Military AI:

- Project Maven: AI for intelligence analysis and drone operations

- JEDI Cloud: Military cloud computing with AI capabilities

- Autonomous Weapons: Ethical AI warfare development

Chinese Military AI:

- Military-Civil Fusion: Integration of civilian AI development with military applications

- Surveillance State: AI-powered monitoring and social control systems

- Cyber Warfare: AI-enhanced offensive and defensive cyber capabilities

Economic Impact and Market Dynamics

Job Market Transformation

U.S. Labor Market:

- Job Creation: New AI-related roles in research, development, and implementation

- Job Displacement: Automation affecting manufacturing and service sectors

- Skill Premium: Increasing wages for AI-capable workers

Chinese Labor Market:

- Manufacturing Automation: Rapid deployment of AI in factories

- Service Sector AI: Extensive use in retail, finance, and logistics

- Education Investment: Massive retraining programs for AI economy

Industry Transformation Patterns

| Sector | U.S. Leadership Areas | Chinese Leadership Areas |

|---|---|---|

| Healthcare | Drug discovery, medical devices | Medical imaging, telemedicine |

| Finance | Algorithmic trading, fintech | Mobile payments, digital banking |

| Transportation | Autonomous vehicle software | Electric vehicle manufacturing |

| Manufacturing | Design and optimization | Factory automation, robotics |

| Entertainment | Content generation, gaming | Social media algorithms, streaming |

Challenges and Vulnerabilities

United States Challenges

Infrastructure Limitations:

- Power Grid: AI computing demands strain electrical infrastructure

- Talent Shortage: Growing gap between AI talent demand and supply

- Regulatory Uncertainty: Unclear long-term AI governance framework

Competitive Pressures:

- Cost Competition: Chinese AI services offered at lower prices globally

- Speed of Deployment: Slower implementation due to regulatory and privacy concerns

- Market Access: Chinese market largely closed to US AI companies

Chinese Challenges

Technology Dependencies:

- Semiconductor Reliance: Critical dependence on foreign chip technology

- Software Ecosystem: Limited access to cutting-edge US AI development tools

- Talent Retention: Brain drain to US companies and universities

Systemic Limitations:

- Innovation Culture: Less emphasis on breakthrough research vs. implementation

- Global Trust: Privacy and surveillance concerns limit international adoption

- Regulatory Isolation: Increasing separation from Western technology ecosystems

Future Scenarios: Potential Outcomes

Scenario 1: Continued U.S. Leadership (35% Probability)

Driving Factors:

- Breakthrough in AI hardware or algorithms

- Successful immigration and talent attraction policies

- Effective alliance building with democratic nations

- Chinese technological isolation due to sanctions

Key Indicators:

- US companies maintain 60%+ market share in foundation models

- Silicon Valley continues to attract top global AI talent

- Democratic AI standards become global norm

Scenario 2: Chinese Technological Leapfrog (25% Probability)

Driving Factors:

- Successful domestic semiconductor development

- Breakthrough in AI efficiency or novel architectures

- Effective state-directed innovation coordination

- US brain drain or reduced investment

Key Indicators:

- Chinese AI models achieve parity or superiority

- Domestic chip production meets AI computing needs

- Global South adopts Chinese AI standards

Scenario 3: Bipolar AI World (40% Probability)

Driving Factors:

- Technological decoupling continues

- Both countries maintain distinct advantages

- Regional bloc formation around AI standards

- Innovation continues in both ecosystems

Key Indicators:

- Separate AI development ecosystems emerge

- Regional preferences for US vs. Chinese AI systems

- Limited technology transfer between blocs

Strategic Implications for Businesses and Investors

For Global Corporations

Strategic Considerations:

- Technology Stack Decisions: Choose AI platforms with long-term viability

- Market Access: Navigate restrictions and regulatory requirements

- Talent Strategy: Compete for scarce AI expertise globally

- Supply Chain: Manage semiconductor and technology dependencies

For Investors

Investment Opportunities:

- AI Infrastructure: Computing, storage, and networking companies

- Vertical AI Applications: Industry-specific AI solutions

- AI Safety and Security: Growing market for AI governance tools

- Alternative Architectures: Quantum computing and edge AI technologies

For Governments

Policy Priorities:

- Talent Development: Education and immigration policies for AI workforce

- Research Investment: Public funding for basic AI research

- Ethical Framework: Responsible AI development guidelines

- International Cooperation: Alliance building and standard setting

The Path Forward: Cooperation vs. Competition

Areas for Potential Cooperation

Global Challenges:

- Climate Change: AI applications for environmental monitoring and sustainability

- Healthcare: Pandemic response and global health initiatives

- Safety Research: AI alignment and existential risk mitigation

- Standards Development: Technical interoperability and safety standards

Competitive Boundaries

National Security Areas:

- Military AI: Defense applications remain firmly competitive

- Surveillance Technology: Competing models of privacy vs. security

- Critical Infrastructure: AI systems for power grids, communications

- Semiconductor Technology: Core strategic technology competition

Conclusion: A Race with Multiple Winners

The U.S.-China AI race is not a zero-sum competition with a single winner. The United States has an advantage over China in total compute capacity. If used strategically, this could drive economic transformation, secure technological leadership, and shape the global AI ecosystem. However, China’s implementation strengths and massive market provide significant advantages in AI deployment and scaling.

Key Takeaways:

- Complementary Strengths: The US leads in research and innovation; China excels in implementation and manufacturing

- Dynamic Competition: Leadership varies by AI application area and market segment

- Global Impact: The competition benefits global AI advancement through increased investment and innovation

- Multiple Scenarios: Future outcomes depend on policy decisions, technological breakthroughs, and geopolitical developments

The Real Winners: Ultimately, the global AI race may produce multiple winners:

- Consumers: Better AI products and services through competition

- Developing Nations: Access to competing AI technologies and standards

- Global Innovation: Accelerated AI development through competitive pressure

- Humanity: Faster progress on AI applications for global challenges

The U.S.-China AI race is reshaping the global technology landscape, creating both opportunities and challenges for businesses, governments, and individuals worldwide. Success in this competition will require not just technological advancement, but strategic thinking about how AI can create value for society while maintaining security and ethical principles.

As this race continues to evolve, the countries that best balance innovation with responsibility, competition with cooperation, and technological advancement with human values will ultimately shape the AI-powered future we all inhabit.